This analysis report provides a data-driven overview of the current state of the American pharmaceutical retail market. The primary purpose is to identify key trends in market concentration, geographic distribution, and industry health.

The analysis is based on a study of 13 major pharmacy chains, including:

- Albertsons Pharmacy

- CVS Pharmacy

- Genoa Healthcare

- GNC

- Good Neighbor Pharmacy

- Health Mart

- Longs Drugs

- Publix

- Rite Aid

- Safeway Pharmacy

- The Medicine Shoppe Pharmacy

- The Vitamin Shoppe

- Walgreens

Data Source: POI data is sourced from the ScrapeHero Data Store, providing a comprehensive view of 30,145 pharmacy locations across the US. Supplementary market share and revenue data are cited from Statista and IBISWorld.

US Pharmacy Market Size and Growth: A Stable, Billion-Dollar Industry

According to IBIS World, the US pharmacy retail sector remains a colossal market, with revenue projected to grow at a CAGR of 1.1% to $609.6 billion by the end of 2025.

- Key growth drivers include:

- Rising enrollment in private insurance and public programs (Medicare/Medicaid).

- Increased consumer focus on health and wellness.

- Consistent demand for prescription drugs, the sector’s largest product segment.

The market demonstrates stability, with the vast majority of locations operational.

Pharmacy Industry Segmentation in the US: A Tale of Two Tiers

The US retail pharmacy landscape is sharply divided between a few dominant national players and a long tail of regional and specialized chains.

Market Share Segmentation: The Prescription Powerhouses

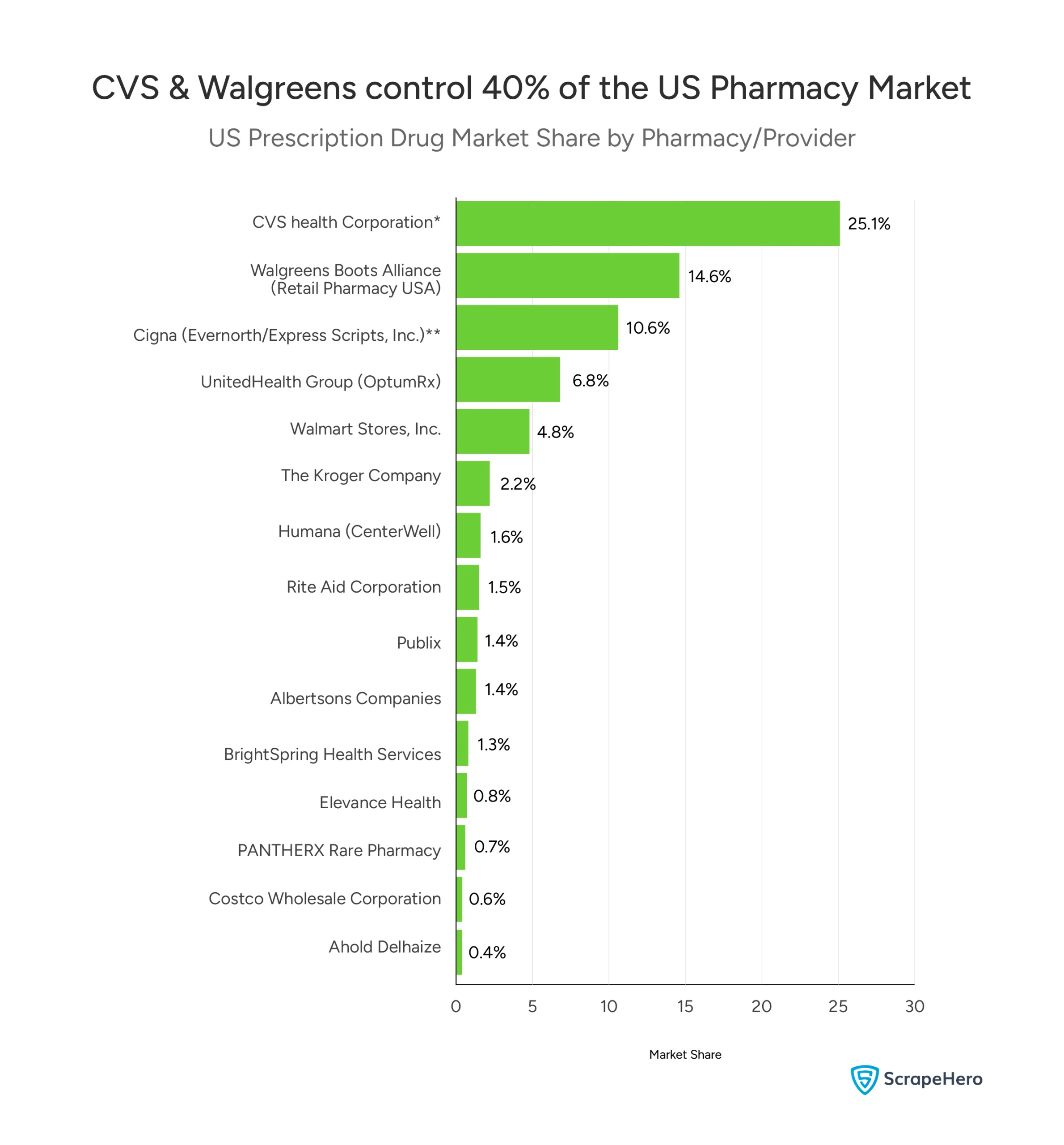

The US pharmacy market is dominated by a powerful duopoly. A clear pharmacy industry segmentation emerges when analyzing prescription drug market share.

CVS Health Corporation is the undisputed leader. It holds a commanding 25.1% share of the US prescription market.

Walgreens Boots Alliance is a strong second with 14.6%. Together, these two retail giants control nearly 40% of the market.

This retail pharmacy market analysis reveals a steep drop after the top two. The third-largest player, Cigna, holds 10.6%. UnitedHealth Group (OptumRx) follows at 6.8%. Walmart Stores, Inc. rounds out the top five with 4.8%.

- The top five companies collectively control over 60% of the total prescription drug market share.

- This highlights an extreme concentration of revenue among a handful of firms.

- The remaining market is fragmented among many smaller chains.

This concentration has major implications. It influences everything from drug pricing to consumer access.

The US pharmacy market analysis shows that competition primarily exists between these giants and their specialized service offerings, not on store count alone.

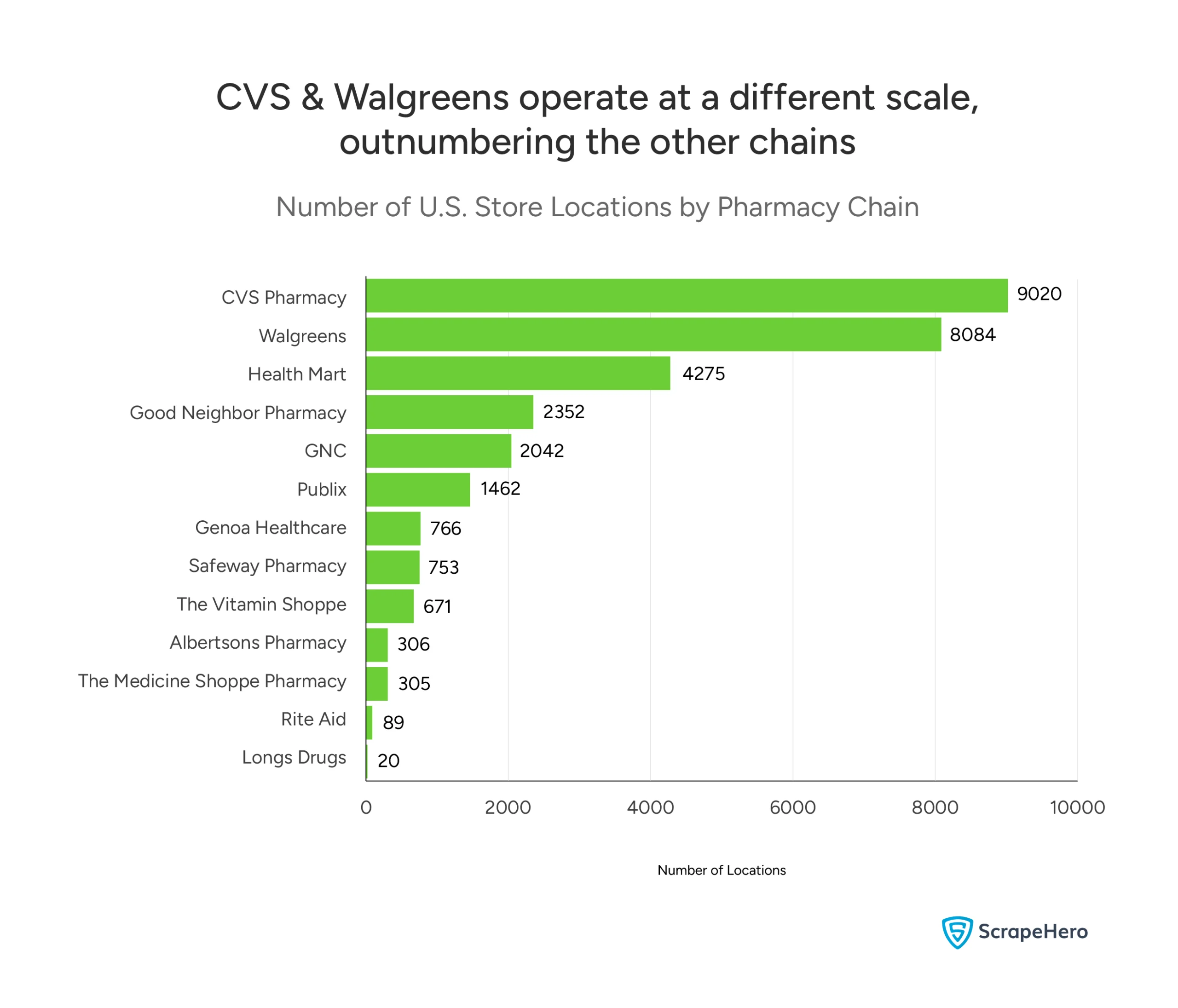

Physical Footprint Segmentation: Store Count Leaders

Analyzing the US pharmacy market by store count reveals a clear tiered structure.

CVS Pharmacy and Walgreens define the top tier. They operate on a scale unmatched by their competitors.

- CVS Pharmacy leads with 9,020 locations.

- Walgreens follows closely with 8,084 locations.

These two chains alone account for over half of the total locations studied in this pharmacy market analysis. The gap to the next largest chain is immense.

Want to compare the locations of these giants?

Download the complete list of all CVS Pharmacy locations in the US and all of Walgreens’ locations now!

The second tier consists of chains with a significant, but far smaller footprint.

- Health Mart operates approximately 4,275 stores.

- Good Neighbor Pharmacy has about 2,352 locations.

- GNC follows with roughly 2,042 stores.

This pharmacy industry segmentation shows a steep drop after the top six. Chains like Publix, Genoa Healthcare, and Safeway form a third tier.

This store count analysis confirms that physical access to pharmacies for most Americans is provided by just two companies: CVS and Walgreens.

The US pharmacy market size in terms of locations is vast. But its distribution is highly unequal.

Retail Pharmacy Market Analysis: Key Competitive Dynamics

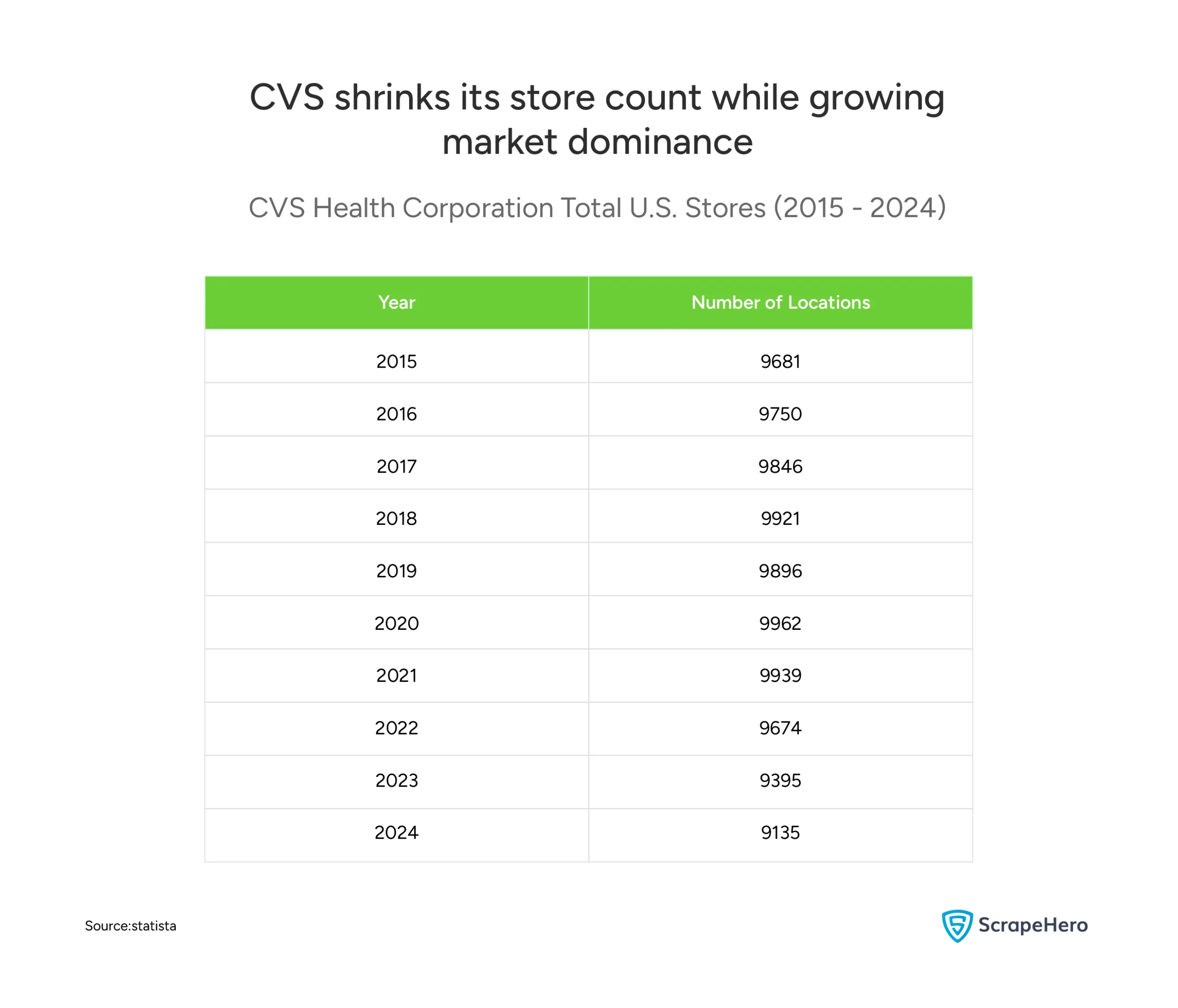

Is the Market Consolidating? The CVS Case Study

CVS has consistently reduced its number of physical stores over the past decade. This trend occurred even as the company solidified its position as the market share leader.

- CVS operated 9,681 stores in 2015.

- This number peaked at 9,962 stores in 2020.

- By 2024, the count had fallen to 9,135 stores.

This represents a net reduction of 546 stores over the nine-year period. This retail pharmacy market analysis reveals a crucial insight. Growth in the US pharmacy industry is no longer just about opening more doors.

So, why would the market leader close stores? This strategy points to a deeper pharmacy industry segmentation and consolidation trend.

- Focus on Profitability: CVS might be optimizing its network, closing underperforming locations to improve overall margins.

- Strategic Consolidation: A move to strengthen core markets rather than maintain a diffuse national footprint.

This case study is key to understanding the current US pharmacy market analysis. The market is maturing. The winning strategy is evolving from physical expansion to operational excellence and service integration.

- The top players are not necessarily trying to have a store on every corner.

- They are working to make each store more valuable and integrated into a broader healthcare ecosystem.

This trend suggests a future where retail pharmacy market success depends on a mix of convenient access, clinical services, and efficient operations.

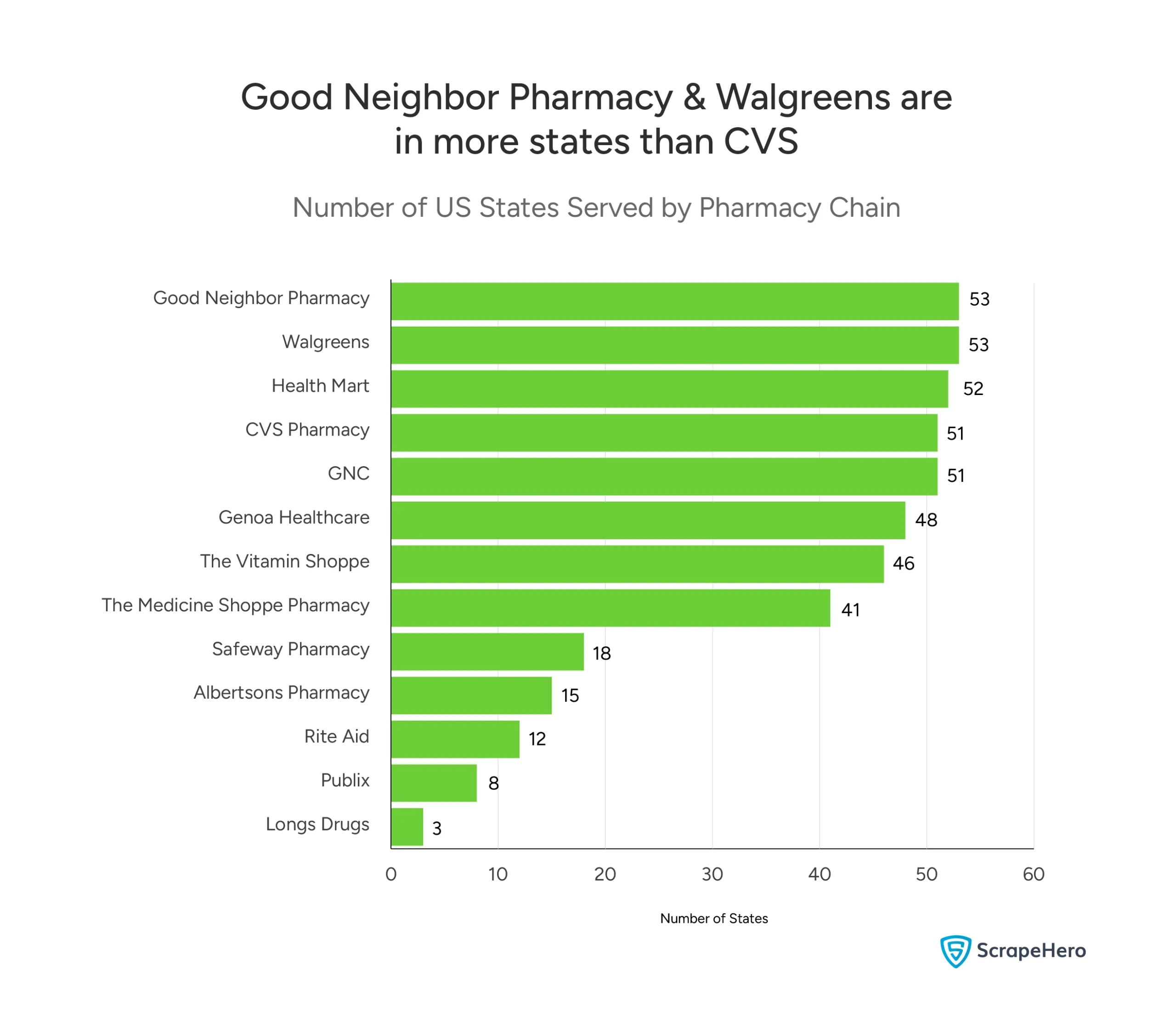

Geographic Penetration: Which Chains Have the Widest Reach?

A key part of pharmacy industry segmentation is geographic coverage. Which chains are truly national, and which are regional? This US pharmacy market analysis looks at state-level presence to answer that.

The data reveals that the chain with the most stores is not always the one with the widest geographic reach.

- Good Neighbor Pharmacy and Walgreens operate in 53 states each (including territories like D.C. and Puerto Rico). They have the broadest national footprint.

- Health Mart is present in 52 states, showing it is also a near-ubiquitous national network.

- CVS Pharmacy and GNC serve 51 states each, confirming their status as truly national chains.

This retail pharmacy market analysis shows that widespread state coverage is common among the top players. It might be a baseline requirement for national competition.

- Chains like Genoa Healthcare (48 states) and The Vitamin Shoppe (46 states) also have extensive, though not complete, national distribution.

- This contrasts with regional grocers and retailers. For example, Publix is only in 8 states and Safeway is in 18. Their pharmacy market presence is concentrated in specific regions.

This segmentation is important for understanding the US pharmacy industry.

- For Consumers: It means brands like Walgreens, CVS, and Good Neighbor Pharmacy are accessible almost anywhere in the country.

- For Competition: It shows that national competition is largely between these widely distributed franchises and chains, not regional grocers.

The US pharmacy market is national in scope for its leading players. But significant regional retail pharmacy market segments still thrive under different brand names.

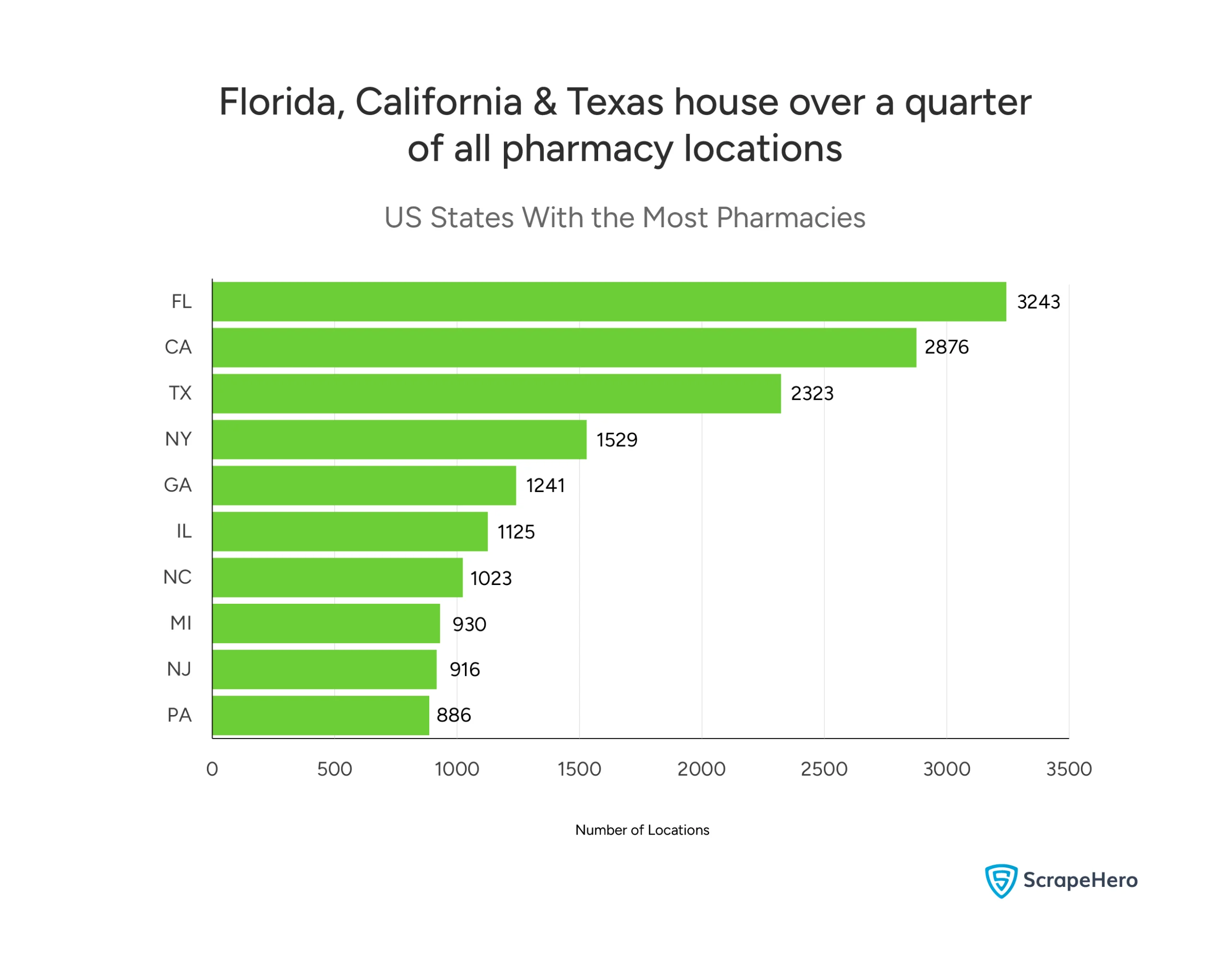

Where Are the Pharmacies? A Geographic Examination

Which States Have the Most Pharmacy Locations?

The US pharmacy market is not evenly distributed. This retail pharmacy market analysis of state-level data reveals where the industry concentrates its physical presence.

Three states dominate the landscape by a wide margin. Together, they account for a massive portion of the national total.

- Florida leads the nation with 3,243 pharmacy locations.

- California follows closely with 2,876 locations.

- Texas holds third place with 2,323 locations.

This top trio alone represents over 8,400 stores. That is more than a quarter of all locations in this US pharmacy market analysis.

- New York (1,529) and Georgia (1,125) round out the top five states.

- Other major markets include Illinois (1,023), North Carolina (930), and Michigan (916).

Understanding this geographic distribution is key. It shows that the retail pharmacy market is deeply embedded in America’s most populous regions. Success in the US pharmacy market is often defined by performance in these key states.

Who Leads in Key State Markets?

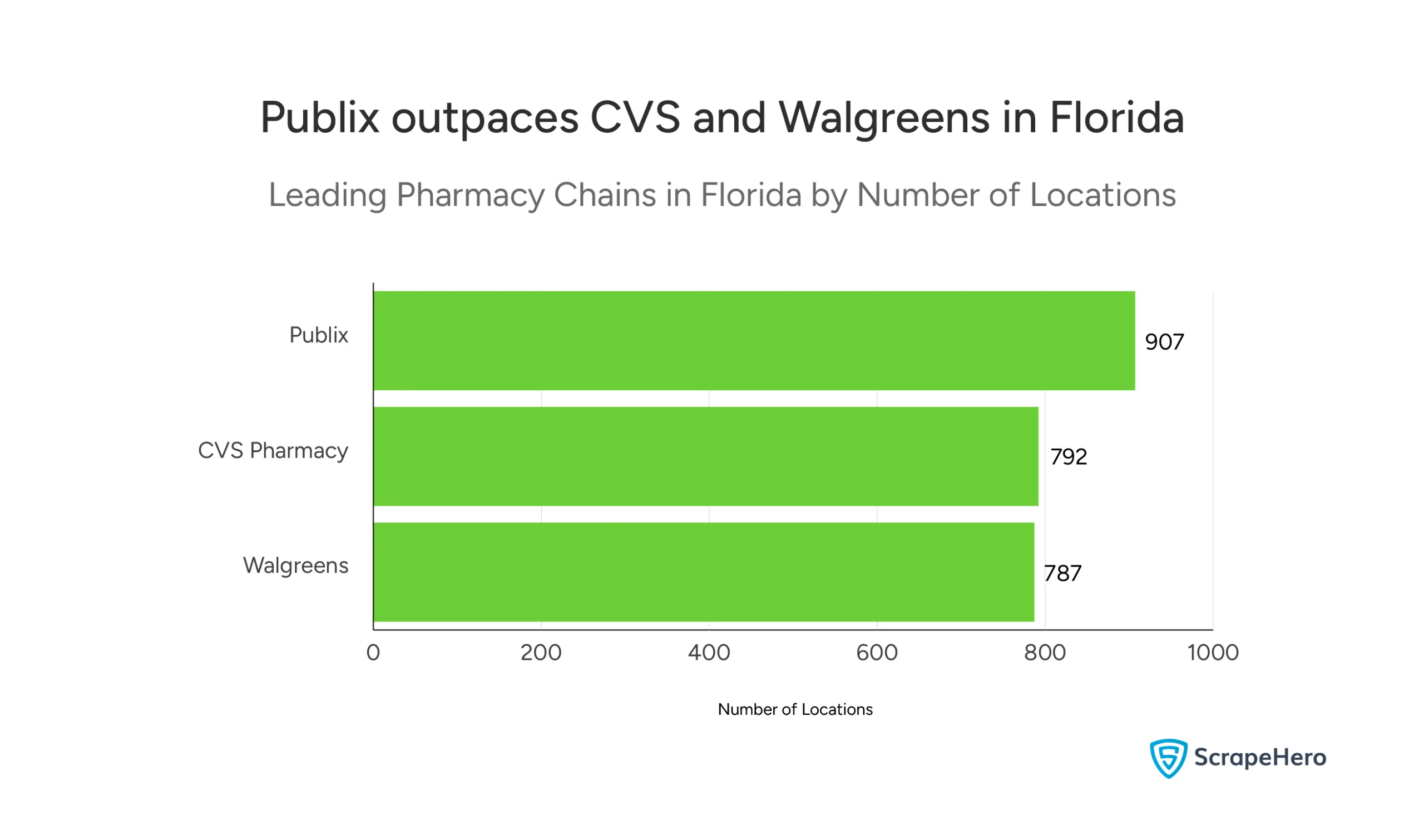

Florida is the largest pharmacy market in the US by store count. The competition there is fierce and surprising.

- Publix is the leading pharmacy chain in Florida with 907 locations.

- CVS Pharmacy follows closely with 792 stores.

- Walgreens holds third place with 787 locations.

This reveals a crucial insight for pharmacy industry segmentation. A regional grocery chain can outperform dedicated national pharmacy leaders in its home market.

This state-level analysis is essential to a complete analysis of the US pharmacy market.

- It proves that national scale does not guarantee a #1 position in every regional market.

- It shows that for chains like CVS and Walgreens, competing with strong regional grocers is a major challenge in key states.

Market Health & Outlook: A Stable and Expanding Network

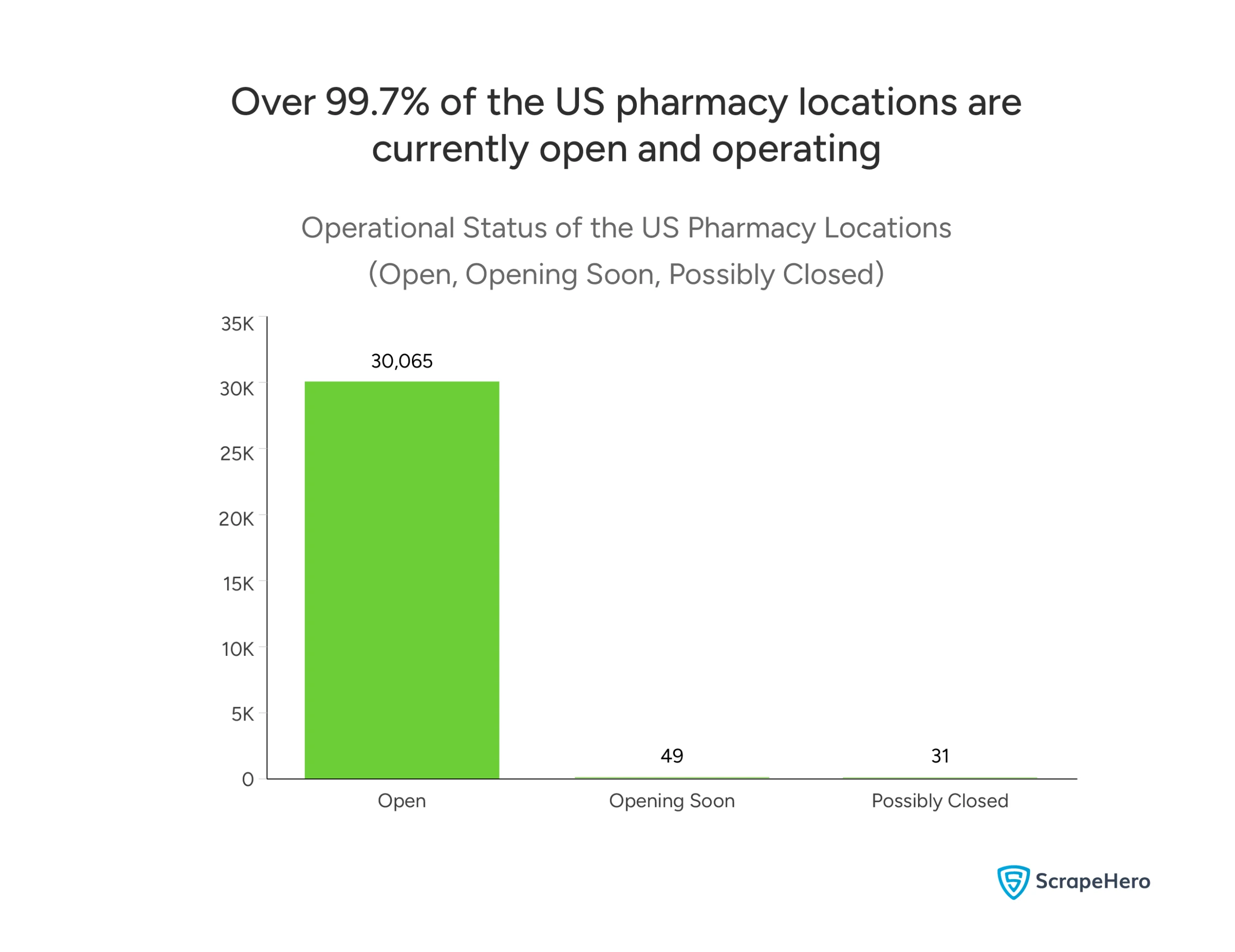

The overall health of the US pharmacy market is strong. The industry shows remarkable stability with very little location turnover. This is a key finding for any retail pharmacy market analysis.

The data on operational status provides a clear snapshot.

- 30,065 pharmacy locations are currently open and serving customers.

- Only 49 locations are listed as “Opening Soon.”

- A mere 31 locations are flagged as “Possibly Closed.”

This means over 99.7% of the tracked network is active. The US pharmacy industry is not in a state of decline or rapid churn. It is a mature and solidly entrenched market.

What does this mean for the US pharmacy market analysis and outlook?

- The network is stable. Consumers can rely on consistent access to pharmacy services in their communities.

- Growth is incremental. Expansion is happening slowly, with only a handful of new stores opening relative to the massive existing base.

- Closures are minimal. This indicates that most pharmacy locations are economically viable, even with intense competition.

This stability supports the positive US pharmacy market size and growth projections.

- The market is not shrinking. It is consolidating and optimizing for efficiency, as seen in the CVS case study.

- The low number of “opening soon” locations suggests chains are focused on optimizing existing stores rather than aggressive nationwide expansion.

- The pharmacy industry segmentation is settled, with established players maintaining their networks.

In conclusion, the US pharmacy market is in a healthy, steady state. It is a reliable and essential piece of the national healthcare infrastructure, poised for measured, service-driven growth rather than disruptive change.

Conclusion: Summary of the US Pharmacy Retail Landscape

The US pharmacy market is a story of immense scale, stark concentration, and strategic evolution. This comprehensive retail pharmacy market analysis, based on location and market share data, paints a clear picture of a mature yet steadily growing industry.

The market is a stable, billion-dollar giant, projected to reach $609.6 billion in revenue by 2025. It is underpinned by consistent demand, an aging population, and broad insurance coverage. Its operational health is robust, with over 99.7% of locations currently open—a testament to its essential role in the healthcare ecosystem.

However, this stability exists within a framework of extreme consolidation. The pharmacy industry segmentation reveals a dominant duopoly:

- CVS Health and Walgreens collectively control nearly 40% of the prescription drug market share.

- Together, they operate over 17,000 stores, providing physical access to a majority of Americans.

- The top five companies command over 60% of the market, creating a high barrier to entry and concentrating tremendous influence over drug pricing and distribution.

Beyond national market share, competition plays out distinctly at the local level. Our geographic analysis uncovered key insights:

- The market is heavily concentrated in populous states like Florida, California, and Texas, which house over a quarter of all locations.

- While CVS and Walgreens have nationwide footprints, regional powerhouses like Publix can lead in critical markets (e.g., Florida), proving that local brand strength and integrated retail are powerful competitive advantages.

- The leading strategy is shifting from pure footprint expansion to network optimization and service integration, as evidenced by CVS strategically reducing its store count while growing its market dominance.

The future of the retail pharmacy market will be defined not by who has the most stores, but by who can most effectively blend convenient access with valuable healthcare services, all while navigating the complexities of a highly concentrated and competitive landscape.

The market is settled, stable, and strategically pivoting to meet the next wave of consumer and healthcare demands.

But here’s the question!

Are You Wondering How to Do a Similar Analysis?

The reality is that analyzing any industry requires data at scale. You would need store counts in every state, pricing from multiple e-commerce platforms, product category breakdowns, and customer ratings—all current, accurate, and structured for analysis.

This is where a web scraping service becomes invaluable.

Instead of manually visiting hundreds of store locator pages or checking prices across platforms, the data arrives ready for analysis.

For businesses that need similar market intelligence, a web scraping service like ScrapeHero handles the heavy lifting: navigating complex websites, extracting data at scale, ensuring accuracy, maintaining updates, and delivering information in usable formats.

No software to install, no technical expertise required, no time spent on data collection.

The alternative, building an in-house scraping operation or manually gathering data, means diverting resources from what actually matters: analyzing the market and making strategic decisions.

When you need data effortlessly, outsourcing to a specialized web scraping service is simply the smarter choice. You get the insights without the infrastructure.

Report by ScrapeHero using publicly available data from the ScrapeHero Data Store, Statista, and IBISWorld. This is an independent market analysis and is not affiliated with any pharmacy chains mentioned.