About the Report: This is a market analysis report on UK Convenience Stores, covering industry size, market structure, and the geographic footprint of major chains. It combines industry-level data with a deep dive into 7 specific chains: Premier Stores, Costcutter, One Stop, Best-one, Scotmid Co-operative, Day-Today, and Keystore, which together operate 8,708 stores.

Data Sources:

- Industry-level data sourced from IBISWorld and Mintel.

- Store location data across all seven chains was downloaded from the ScrapeHero Data Store.

What Is the UK Convenience Retail Market Size in 2026?

The UK convenience retail market is large, growing, but not without friction.

According to IBISWorld, revenue was forecast to reach £54.6 billion by 2025–26, growing at a compound annual rate of 0.8% over the five years prior. That’s modest growth. Cost-of-living pressures and price-sensitive shopping habits have kept consumer spending cautious,and that’s reflected in the numbers.

But zoom out to 2029, and the picture looks more optimistic. The market is forecast to grow by over 12% between 2025 and 2029, a signal that the sector has real momentum behind it, even if the short-term gains are slow.

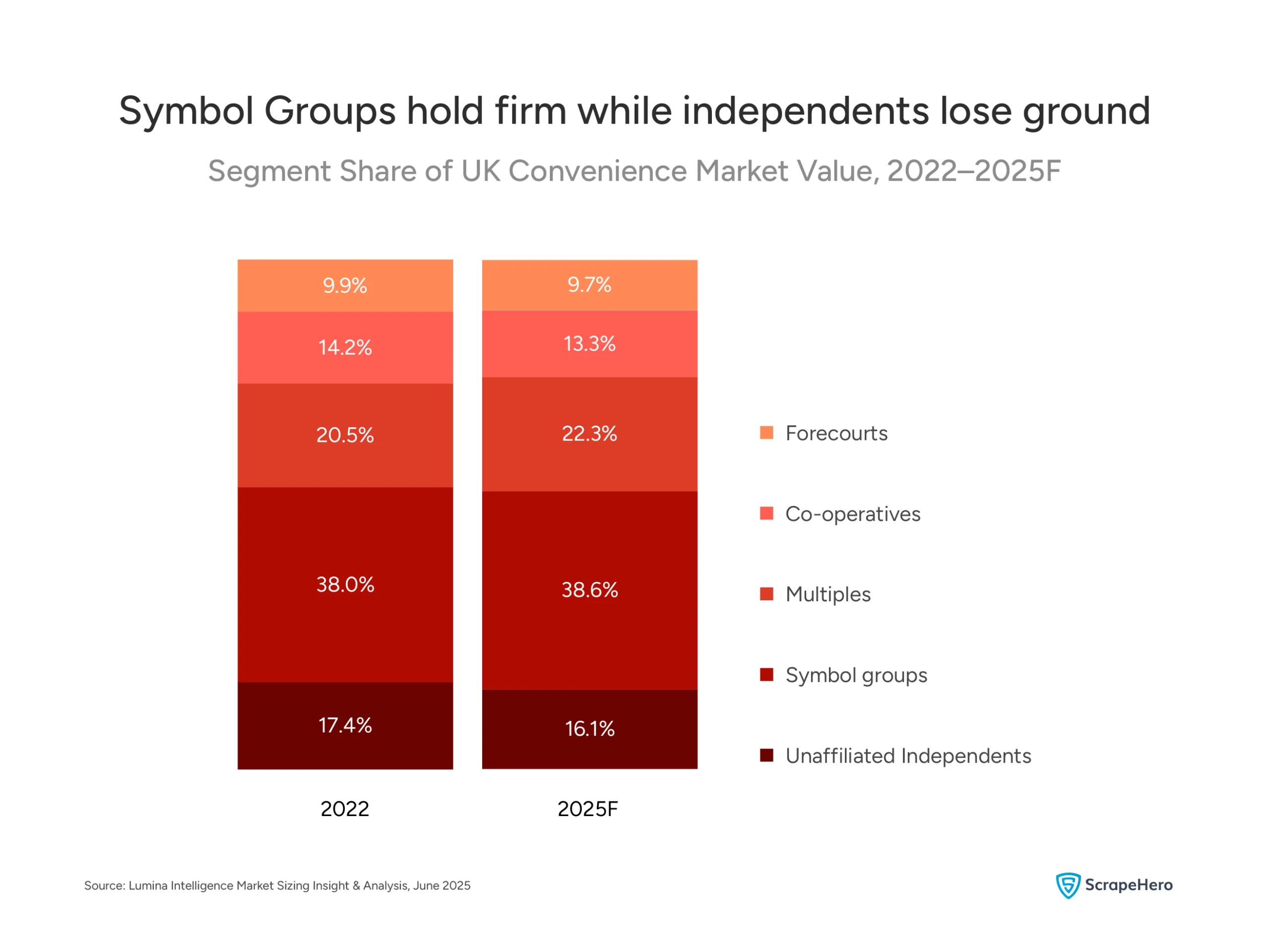

This chart tells the structural story of the market clearly.

- Symbol groups hold the largest share at 38.6%, and have stayed remarkably stable, ticking up slightly from 38.0% in 2022. These are independent stores operating under a shared brand or buying group.

- Multiples are the ones gaining ground, up from 20.5% to 22.3%. These are corporate-owned chains expanding deliberately and consistently.

- Co-operatives are slipping slightly, from 14.2% to 13.3%. Still a significant segment, but losing pace.

- Unaffiliated independents are losing the most, dropping from 17.4% to 16.1%. Without the buying power or brand recognition of a larger group behind them, they’re finding it harder to compete.

- Forecourts remain largely flat, holding at around 9.7%.

The overall direction is clear: the market is shifting toward organised, larger retail groups.

How Is the UK Convenience Retail Market Structured?

The segment data tells us who controls the market broadly.

But to understand what that looks like on the ground, store by store, city by city, you need to look at the chains themselves.

Before we get there, one segment worth addressing separately:

What Role Do Forecourts Play in UK Convenience Retail?

Forecourts (convenience retail attached to petrol stations) account for roughly 9.7% of market value in 2025, a minor dip from 9.9% in 2022.

They’re a stable part of the market, but not a growing one. The data doesn’t point to forecourts as a significant driver of market expansion — at least not within the scope of this analysis.

Which Convenience Retailers Are Expanding Fastest in the UK?

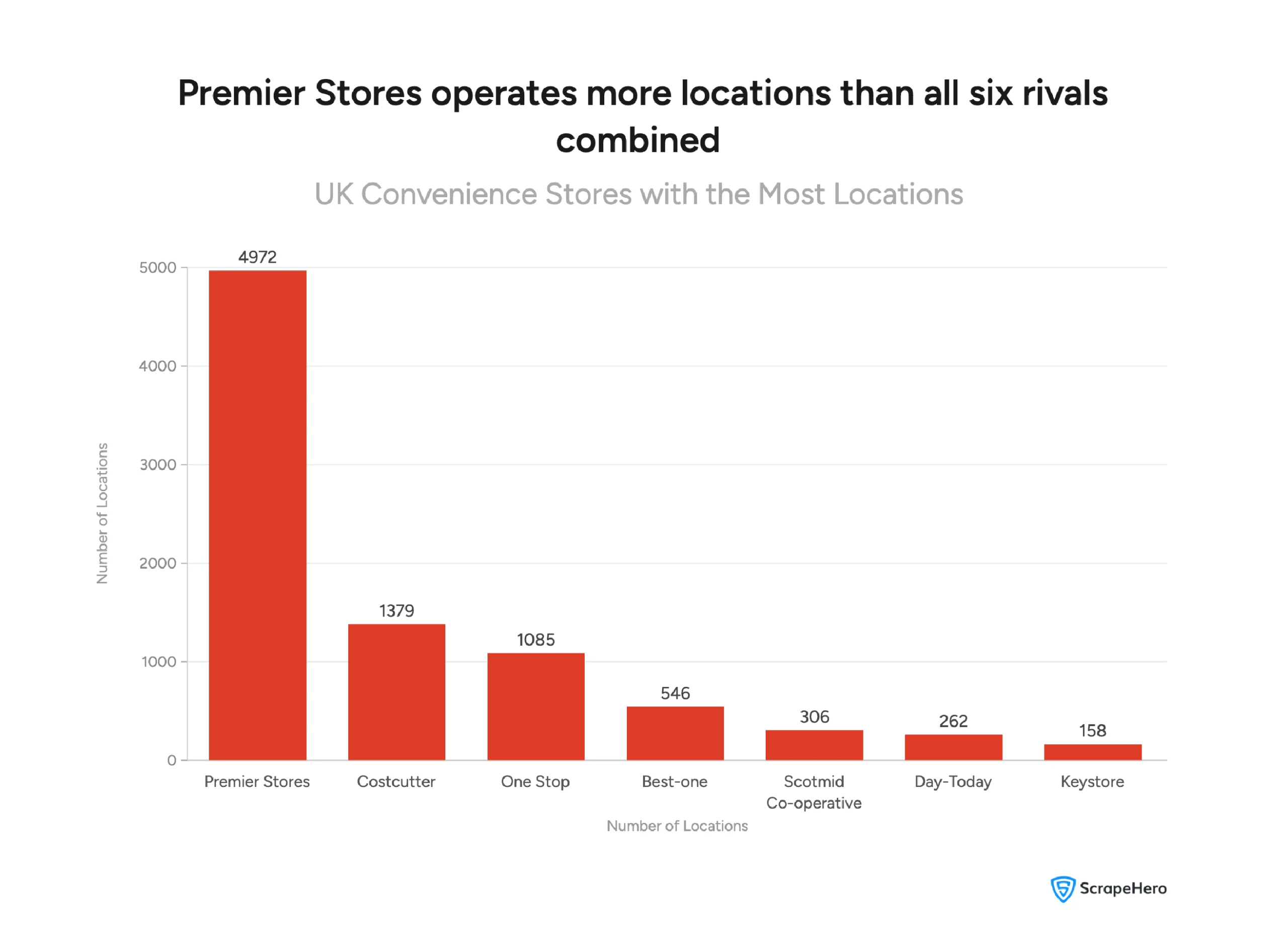

Seven chains define a significant portion of the UK convenience retail landscape. Between them, Premier Stores, Costcutter, One Stop, Best-one, Scotmid Co-operative, Day-Today, and Keystore, they account for 8,708 store locations across the country.

But the distribution of those locations is far from even.

Premier Stores dominates by a significant margin. With 4,972 locations, it operates more stores than the other six chains combined. That’s a structural advantage that shapes how the entire sector operates.

Want the complete list of all Premier Stores locations in the UK?

The rest of the market breaks into two clear tiers:

Mid-tier chains:

- Costcutter — 1,379 locations

- One Stop — 1,085 locations

- Best-one — 546 locations

Smaller, more focused operators:

- Scotmid Co-operative — 306 locations

- Day-Today — 262 locations

- Keystore — 158 locations

The gap between Premier Stores and everyone else is the defining feature of this market. This is a highly uneven competitive landscape.

Premier Stores is owned by Booker Group — the UK’s largest food wholesaler, itself acquired by Tesco in 2018. That ownership gives Premier Stores access to Tesco’s supply chain, buying power, and distribution network. It’s a significant structural advantage that helps explain the scale gap between Premier and every other chain in this analysis. Source: Booker Group | Tesco PLC

But store count alone doesn’t tell the full story. Where those stores are and how spread out they are reveals just as much about each chain’s strategy.

Which UK Regions Have the Highest Convenience Store Density?

England accounts for the overwhelming majority of convenience store locations- 6,495 stores across the seven chains studied.

Scotland follows with 1,420, and Wales with 674.

Northern Ireland has just 113, and the Isle of Man and Channel Islands have negligible presence.

But the more revealing figure is the average distance between stores within each region:

- England — 1.61 km

- Scotland — 1.75 km

- Wales — 1.89 km

- Northern Ireland — 4.04 km

- Isle of Man — 7.74 km

In England, stores are close together; competition is high, and access is easy.

In Northern Ireland and the Isle of Man, the gaps are significantly larger. These are underserved markets.

For any retailer or supplier thinking about where whitespace exists in the UK convenience sector, these figures are a useful starting point.

Two Strategies, Seven Chains

Looking at regional coverage — not just store count — reveals two very different approaches to expansion.

Costcutter operates across 5 regions: England, Scotland, Wales, Northern Ireland, and the Isle of Man. It has the widest geographic reach of any chain in this analysis.

Best-one and Premier Stores each cover 4 regions — broad national presence, but slightly less reach than Costcutter.

One Stop and Scotmid cover 3 regions each — selective but meaningful presence.

Keystore operates across 2 regions — England and Scotland only.

Day-Today operates in Scotland alone — a deliberate, concentrated regional strategy.

Two clear approaches emerge:

- National breadth — Costcutter prioritises being present across as many regions as possible, even if store count is lower than Premier Stores.

- Regional depth — Day-Today goes all-in on one market, building density within a single region rather than spreading thin.

Neither strategy is inherently better. But the contrast highlights how differently operators are approaching growth within the same sector.

How Are UK Grocery Retailers Using Location Intelligence?

The store count and regional data in this analysis aren’t just numbers — they reveal how each chain thinks about growth.

- Premier Stores is present in 1,082 cities. No other chain comes close.

- Costcutter follows with 787 cities.

- After that, the drop is sharp — One Stop covers 444 cities, Best-one 329.

- Keystore, Scotmid, and Day-Today all sit just above 100.

That gap between Premier Stores and the rest points to a deliberate strategy: maximum accessibility. Being present in as many towns and cities as possible, rather than concentrating in a few.

Costcutter takes a different approach. Fewer locations than Premier Stores, but the widest regional spread — present across 5 regions, including the Isle of Man and Northern Ireland, where most other chains haven’t ventured.

Day-Today sits at the opposite end. 102 cities. One region. Scotland only. That’s not a limitation — it’s a choice. Deep presence in a single market rather than thin coverage across many.

Two strategies. Very different bets.

The regional density data adds another layer. England’s stores sit an average of 1.61 km apart — a competitive, well-served market. Northern Ireland’s average gap is 4.04 km. The Isle of Man’s is 7.74 km. As the data itself notes, “some regions are still underserved and may have room for expansion.”

Insights like these don’t emerge from guesswork. They come from structured, reliable location data gathered across seven chains and thousands of store locator pages. The store-level data powering this analysis was downloaded from the ScrapeHero Data Store.

What this UK Convenience Retail Market Analysis Reveal

The UK convenience retail market is growing — but the data reveals a sector in transition, not in cruise control.

A few things stand out clearly from this analysis:

- The market is consolidating. Symbol groups and multiples are strengthening their position. Unaffiliated independents are losing share.

- Scale is uneven. Premier Stores operates more locations than the other six chains in this analysis combined.

- Geography matters. England is dense and competitive. Northern Ireland and the Isle of Man have significantly larger gaps between stores, and the data flags these as underserved.

- Strategy varies. Costcutter prioritises regional breadth. Day-Today goes deep in one market. Premier Stores focuses on city-level accessibility.

Disclaimer: The data used in this report is sourced from publicly available information. This analysis has been produced independently by ScrapeHero and is not affiliated with, endorsed by, or produced in association with any of the UK convenience retail market brands. All brand names are the property of their respective owners.

Ready to Understand the UK Market Better?

ScrapeHero is one of the top 3 web scraping services globally, and unlike most data services, we are fully managed. That means real experts handle your data requirements from start to finish, no technical expertise needed on your end.

In an age where AI drives most of the process, ScrapeHero keeps a human involved at every step — from the initial conversation about your requirements to manual QA before delivery. You get clean, structured, trustworthy data without having to chase it yourself.

Frequently Asked Questions About the UK Convenience Retail Market

Premier Stores, with 4,972 locations across the UK. That’s more than the other six chains in this analysis combined — Costcutter (1,379), One Stop (1,085), Best-one (546), Scotmid Co-operative (306), Day-Today (262), and Keystore (158).

England, by a significant margin. Across the seven chains studied, England accounts for 6,495 store locations — more than four times Scotland’s 1,420 and nearly ten times Wales’ 674.

Costcutter, operating across 5 regions — England, Scotland, Wales, Northern Ireland, and the Isle of Man. Despite having fewer total locations than Premier Stores, it has the broadest geographic spread of any chain in this analysis.

The data points to Northern Ireland and the Isle of Man as the most underserved. The average distance between stores in Northern Ireland is 4.04 km — more than double England’s 1.61 km. The Isle of Man’s average is even wider at 7.74 km.

Both are significant segments, but they’re moving in different directions. Symbol groups — where independent store owners operate under a shared brand or buying group — hold the largest share of the market at 38.6%. Multiples, which are corporate-owned chains, are the fastest growing segment, up from 20.5% in 2022 to 22.3% in 2025.

This analysis doesn’t cover shopper behaviour directly. However, outside research suggests that cost-of-living pressures have shifted shopping habits toward smaller, more frequent top-up trips. See the editor’s note earlier in this blog for more context, with sources linked.