About the Report: This report analyzes the structure, scale, and competitive dynamics of Australia’s grocery retail market. It covers store distribution, city coverage, operating hours, pricing, revenue trends, and the regulatory forces reshaping the sector in 2026.

Note: The point-of-interest data used in this analysis, including store locations, city coverage, and operating hours for Woolworths, Coles, ALDI, and IGA, was sourced from the ScrapeHero Data Store.

Overview

Australian supermarkets aren’t just shops. They’re a daily habit for millions of people — and a hotly contested political and economic battleground.

From pricing scandals to a landmark government inquiry, the grocery sector has rarely been under more scrutiny than it is right now. This analysis breaks down who controls the market, how prices are shifting, and what’s actually changing in 2026.

Key Highlights

- Woolworths is the market leader — 2,220 stores across 1,404 cities, with the longest average trading hours at 14.4 hours per day.

- Woolworths and Coles dominate — Woolworths and Coles together control 67% of national grocery sales, leaving limited room for rivals to compete at scale.

- ALDI punches above its weight — with just 609 stores, it offers the cheapest grocery basket in the country at $72.41 for 20 common items.

- Revenue is growing — monthly sector revenue climbed from $11.8 billion in March 2024 to $12.3 billion by March 2025.

- But so are prices — grocery CPI rose across every category, with meat and seafood up 4.4% and fruit and vegetables up 4%.

- Regulators are stepping in — the ACCC’s 2025 inquiry found Australia’s major supermarkets among the most profitable in the world, triggering 20 reform recommendations.

Who are the Biggest Supermarket Chains in Australia?

Australia’s grocery market is effectively a four-player game. Woolworths, Coles, ALDI, and IGA account for the overwhelming majority of the country’s supermarket activity — but they’re not equal players.

Each chain has a distinct strategy, footprint, and customer proposition. Here’s how they stack up.

Australia’s Top Four Supermarkets- A Quick Snapshot

- Woolworths is Australia’s largest supermarket chain by every measure — stores, city coverage, and market share. It operates as a full-service retailer with a wide product range and heavy investment in loyalty programs and convenience.

- Coles is Woolworths’ closest rival and its near-constant companion in the duopoly conversation. With a similar format and customer base, the two chains dominate the sector together.

- ALDI takes a different approach entirely. Fewer stores, fewer products, lower prices — and a growing customer base that keeps coming back for all three.

- IGA is a network of independently owned stores operating under a shared banner, supplied by Metcash.

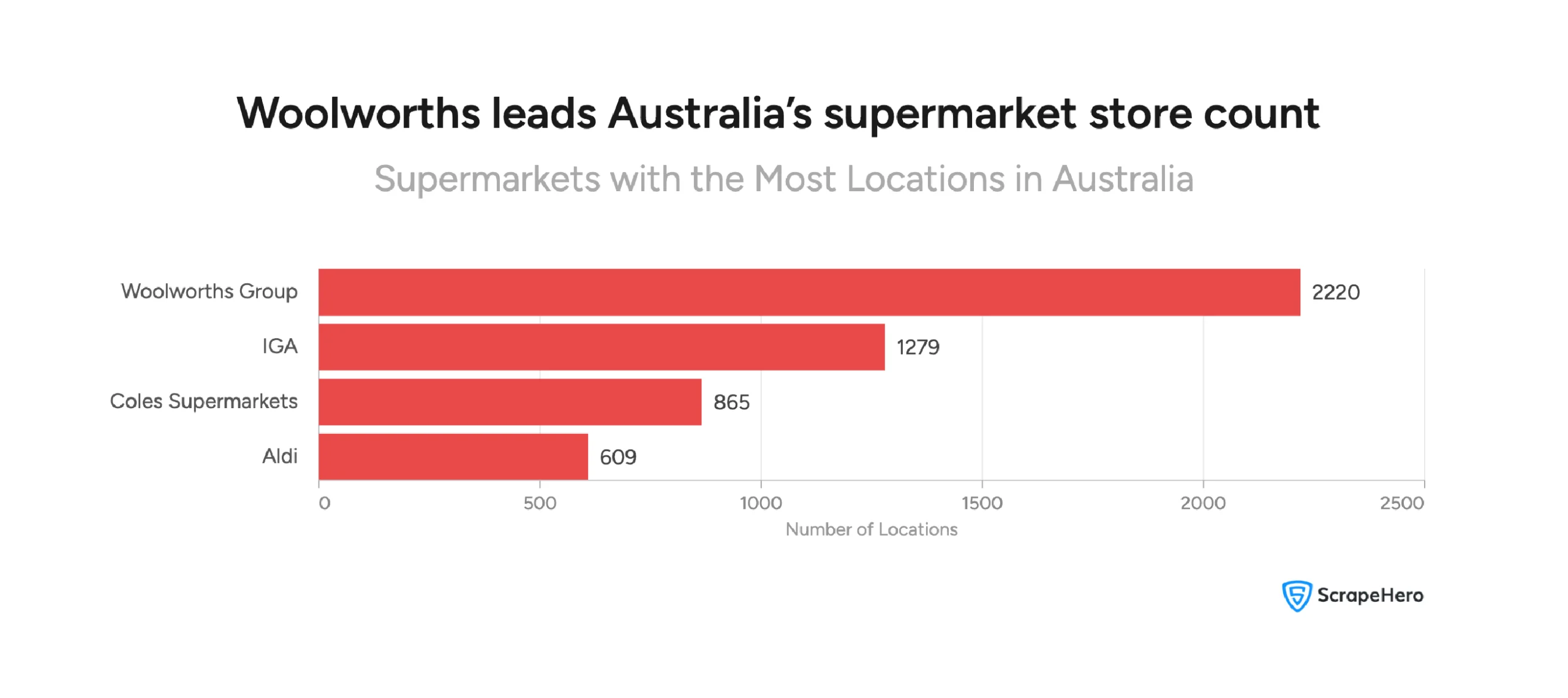

Store Network by the Numbers

When it comes to sheer presence, Woolworths leads by a significant margin.

- Woolworths — 2,220 stores

- IGA — 1,279 stores

- Coles — 865 stores

- ALDI — 609 stores

Easily download the complete list of all Woolworths Group store locations in Australia here!

IGA’s second-place finish might surprise you. But remember — it’s a network of independent retailers, not a single chain.

How far Does Each Chain Actually Reach?

Store count only tells part of the story. City coverage shows how deep into the country each chain actually goes.

- Woolworths — 1,404 cities

- IGA — 1,127 cities

- Coles — 775 cities

- ALDI — 578 cities

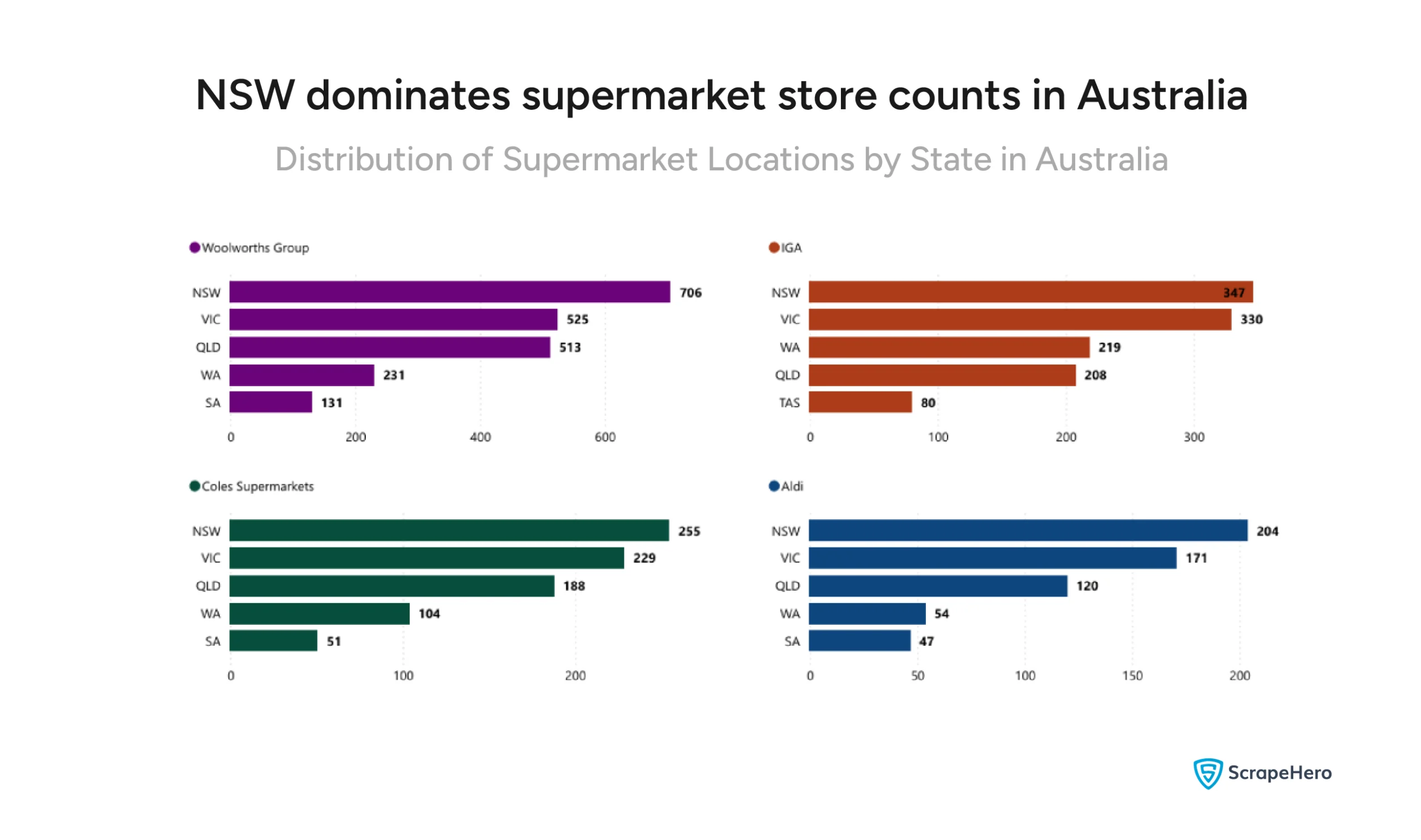

Where are Australia’s Supermarkets Concentrated?

No matter which chain you look at, the pattern is the same — stores cluster along the east and southeast coasts, where Australia’s population is densest.

NSW leads for all four chains:

- Woolworths — 706 stores in NSW

- IGA — 347 stores in NSW

- Coles — 255 stores in NSW

- ALDI — 204 stores in NSW

Victoria and Queensland follow closely.

- Woolworths — 525 in VIC and 513 in QLD

- IGA — 330 in VIC and 208 in QLD

- Coles — 229 in VIC and 188 in QLD

- ALDI — 171 in VIC and 120 in QLD

In Western Australia, Woolworths leads with 231 stores, and IGA follows closely with 219.

What is the Current Size of the Australian Supermarket Industry?

Australia’s grocery sector is big — and getting bigger. Despite cost-of-living pressures squeezing household budgets, consumer spending at supermarkets has continued to climb.

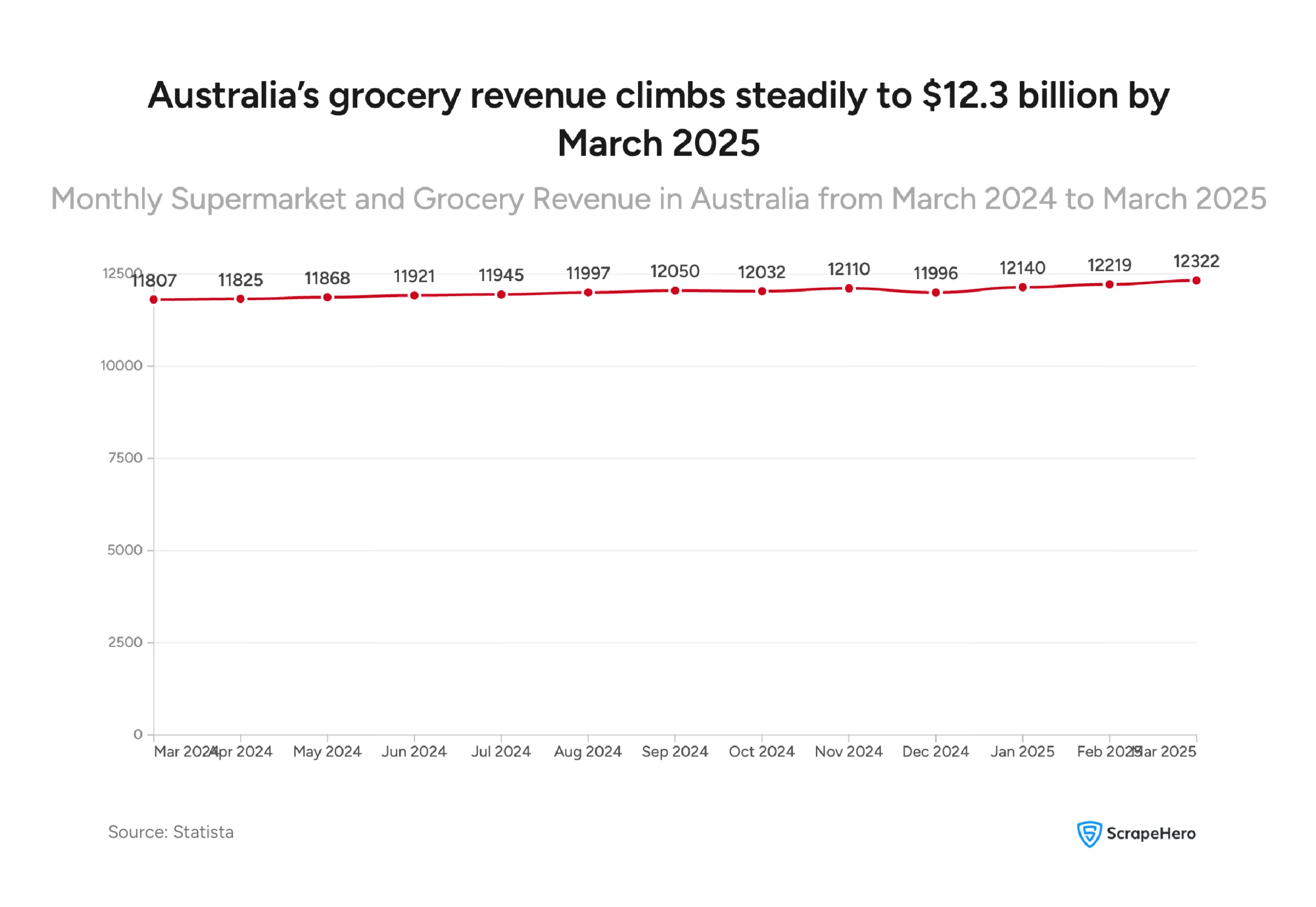

Monthly Revenue Snapshot

Between March 2024 and March 2025, total monthly revenue across Australia’s supermarket and grocery sector grew from $11.8 billion to $12.3 billion — a steady upward trend with only minor dips along the way.

The overall direction is clear — demand for groceries in Australia is stable, consistent, and growing.

Total Sector Profit of the Australian Supermarket Industry in 2026

Revenue tells you how much money flows through the sector. Profit tells you how much stays.

In 2026, Australia’s supermarket and grocery sector recorded $5.6 billion in total profit, according to IBISWorld — a figure that has drawn significant public and regulatory attention given the cost-of-living pressures Australian households have faced over the same period.

What Does This Growth Actually Mean?

Here’s where it gets nuanced. Revenue growth doesn’t always mean more groceries are being sold.

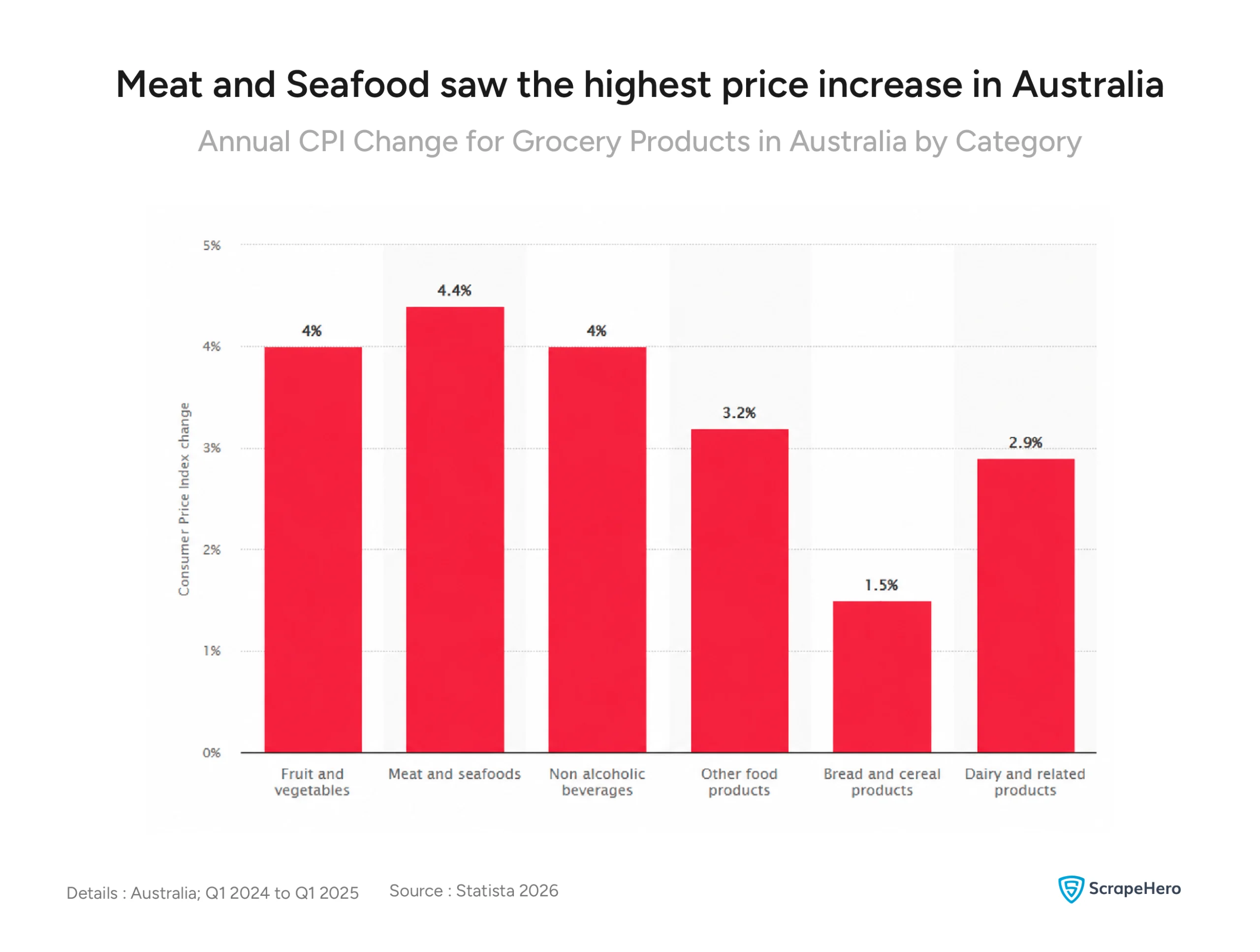

Grocery prices rose across every category between Q4 2024 and Q4 2025, according to Statista — meat and seafood up 4.4%, fruit and vegetables up 4%, and non-alcoholic beverages up 4%. When prices rise, revenue figures rise with them — even if the number of items in shoppers’ baskets stays the same or shrinks.

In other words, some of this growth is real. And some of it might be simply inflation showing up in the numbers.

What is the Market Share of Woolworths vs Coles, and Who Else Competes?

Australia’s grocery market isn’t just concentrated — it’s one of the most concentrated in the developed world. Two companies control two-thirds of it. That’s the starting point for understanding everything else about this sector.

The Numbers Behind the Dominance

According to the ACCC’s 2025 supermarket inquiry, here’s how national grocery sales break down:

- Woolworths — 38%

- Coles — 29%

- ALDI — 9%

- Metcash/IGA — 7%

Woolworths and Coles together account for 67% of national grocery sales. The remaining third is split between ALDI, IGA, and a long tail of smaller independents and specialty retailers.

Why Do Woolworths and Coles Dominate?

It didn’t happen overnight — and it didn’t happen by accident.

Both chains have spent decades building scale advantages that are almost impossible for newcomers to replicate. That includes established supplier relationships, extensive logistics networks, prime retail real estate, and significant investment in customer loyalty programs.

The ACCC’s final report noted that since 2019, Coles and Woolworths have acquired interests in approximately 260 sites intended for future supermarket use — 180 by Woolworths and 80 by Coles. Both chains also hold a significant pipeline of undeveloped and unused sites.

The report observed that their scale and financial resources give them a natural advantage over smaller rivals when competing for prime retail locations. Combined with planning and zoning laws that already limit site availability, this makes large-scale entry into the market considerably more challenging for new competitors.

Is the Australian Grocery Market Actually Competitive?

On paper, four major players sounds like a competitive market. In practice, it’s more complicated.

The ACCC’s inquiry concluded that Woolworths and Coles operate in an oligopolistic market structure with limited incentive to compete vigorously on price. When two players control 67% of the market, the usual competitive pressures that drive prices down are significantly weakened.

That’s not just an academic observation — it’s the central finding that triggered the inquiry’s 20 reform recommendations.

In January 2024, the Australian Government directed the ACCC to conduct a 12-month inquiry into supermarket pricing. The final report, published in March 2025, found that Woolworths and Coles are among the most profitable grocery retailers globally, and that their average product margins had increased over the previous five financial years. Key findings included a significant bargaining power imbalance between the major chains and their suppliers, and concerns around the holding of undeveloped sites that may limit competitor access to prime retail locations. The inquiry made 20 recommendations covering price transparency, supplier protections, and planning reforms.

How Does Pricing Compare Across Australia’s Grocery Chains?

For most Australian households, price is the deciding factor when choosing where to shop. So how big is the gap between the cheapest and most expensive option — and what’s driving grocery prices higher across the board?

Basket Price Comparison of Australia’s Supermarket Giants

Consumer group Choice put this to the test, comparing the cost of a standard basket of 20 common grocery items across all four major chains. The results, excluding specials, were telling:

- ALDI — $72.41

- Woolworths — $98.98

- Coles — $100.04

- IGA — $109.25

That’s a $36.84 gap between the cheapest and most expensive option for the exact same basket of goods. For a household shopping weekly, that difference adds up to over $1,900 a year.

Source: Choice via SBS News

Price Isn’t the Only Differentiator

When prices between Woolworths and Coles are this close, other factors start to matter — and trading hours are one of them.

Average daily operating hours across the four chains tell an interesting story:

- Woolworths — 14.4 hours per day

- IGA — 12.7 hours per day

- Coles — 12.3 hours per day

- ALDI — 11.1 hours per day

Woolworths stores operate the longest on average, with 14.4 hours per day, providing extended shopping access for customers.

How are Grocery Prices Changing in Australia?

Beyond the snapshot comparison, the broader price trend matters too.

Between Q4 2024 and Q4 2025, grocery prices rose across every major product category in Australia, according to Statista:

- Meat and seafood — up 4.4%

- Fruit and vegetables — up 4%

- Non-alcoholic beverages — up 4%

- Other food products — up 3.2%

- Dairy and related products — up 2.9%

- Bread and cereal products — up 1.5%

No category was spared. Staples like bread and dairy — the items most households can’t substitute away from — saw meaningful price increases even at the lower end of the range.

Conclusion

Australia’s supermarket industry is large, profitable, and structurally resistant to disruption. Woolworths and Coles have spent decades cementing advantages — in scale, supplier relationships, logistics, and real estate — that make meaningful competition at the national level exceptionally difficult.

The sector’s revenue growth tells a story of stability and consistent demand. But with grocery CPI rising across every category and $5.6 billion in total profit on the books, the gap between what the market delivers for operators and what it delivers for the broader economy is drawing serious scrutiny.

The ACCC’s 20 recommendations signal a regulatory environment that is tightening — and businesses operating in or adjacent to this sector should watch how those reforms unfold. Pricing transparency mandates, supplier protections, and planning reforms will reshape the competitive landscape in ways that are still becoming clear.

For anyone analysing this market — whether for investment, market entry, supplier strategy, or competitive intelligence — the data points in one consistent direction: this is a high-margin, high-concentration sector where structural change, when it comes, will be slow but consequential.

Disclaimer: The data used in this report is sourced from publicly available information. This analysis has been produced independently by ScrapeHero and is not affiliated with, endorsed by, or produced in association with any of the supermarkets in Australia. All brand names are the property of their respective owners.

Ready to Understand the Australian Market Better?

ScrapeHero is one of the top 3 web scraping services globally, and unlike most data services, we are fully managed. That means real experts handle your data requirements from start to finish, no technical expertise needed on your end.

In an age where AI drives most of the process, ScrapeHero keeps a human at every point — from the first conversation about your requirements to manual QA before delivery. You get clean, structured, trustworthy data without having to chase it yourself.

Frequently Asked Questions About the Australian Supermarket Industry

Australia’s four major supermarket chains are Woolworths, Coles, ALDI, and IGA. Woolworths is the largest by store count, city coverage, and market share, operating 2,220 stores across 1,404 cities. IGA follows with 1,279 stores, Coles with 865, and ALDI with 609.

According to the ACCC’s 2025 supermarket inquiry, Woolworths holds 38% of national grocery sales — the largest share of any single retailer in the country. Coles follows at 29%, giving the two chains a combined share of 67%.

The Australian grocery market is highly concentrated. The ACCC concluded that Woolworths and Coles operate in an oligopolistic market structure with limited incentive to compete vigorously on price. While ALDI provides meaningful price competition where its product range overlaps, significant barriers to entry make large-scale competition from new players unlikely in the short term.

Australia’s supermarket and grocery sector generated over $12.3 billion in monthly revenue as of March 2025, up from $11.8 billion in March 2024. Total sector profit in 2026 stands at $5.6 billion, according to IBISWorld.

Their dominance is the result of decades of scale-building — extensive store networks, established supplier relationships, significant logistics infrastructure, and strong customer loyalty programs. The ACCC also found that both chains hold considerable advantages in securing prime retail sites, making large-scale market entry by new competitors exceptionally difficult.

Based on a basket of 20 common grocery items tested by consumer group Choice, ALDI is the most affordable at $72.41, followed by Woolworths at $98.98 and Coles at $100.04. IGA is the most expensive at $109.25, excluding specials.